For Austrian Banking M&A Deals, ESG Is on the Rise

A conversation with PHH Rechtsanwälte’s Lukas Röper and Victoria Fischl about where Austria’s market is heading.

Tags

Based in Austria, PHH Rechtsanwälte banking and finance partner Lukas Röper, formerly a partner with a Big Four accounting firm, and PHH associate Victoria Fischl, have acted as lead advisors on both the buy- and sell-side. I spoke with them about:

- Where they expect the mergers and acquisitions (M&A) market to go this year

- The rise of environmental, social and corporate governance (ESG) in dealmaking

- How financial institutions can help better facilitate transactions.

SS&C Intralinks: How many Banking M&A deals do you expect to undertake over the next 12 months in Austria?

We expect 2022 to be a very active banking year for M&A. The Austrian Financial Markets Supervisory Authority (FMA) considers Austria to be overbanked in some areas and encourages a further consolidation of the market.

This will likely lead some of the Austrian banking sectors (Raiffeisen, Volksbanken, Sparkassen) to continue merger activity. In these sectors, smaller banks with a regional focus will need to merge in order to reach sustainable balance sheet sizes.

We have also seen several privately owned smaller banks where shareholders are currently considering a sale as a result of increasing regulatory pressure and constrained business opportunities.

Equally, we have had several requests from international investors to conduct market soundings: Investors from outside the European Union (EU), fintechs desiring to grow to the next level and other investors from other industries, which consider a banking platform a benefit for their business model. Austria is becoming an attractive market for banking M&A:

- The private banking sector in Austria is currently underdeveloped, with several market players having reduced their market activities or even withdrawn from the market, hence allowing for ample opportunities for a new strongly service-oriented private wealth bank that will also provide conventional products such as mortgages, loans and deposits. Recent withdrawals include the exit of Credit Suisse and UBS, and the acquisition of Semper Constantia Privatbank by LLB.

- Austria as a Eurozone member has a convenient geographic location. It is a safe financial/banking system with a strong reputation and provides for human talent as well as access to the client base in the center of Europe. Living expenses are favorable as compared to other Western European prime locations such as Frankfurt or Paris.

- Austria has a reputation as a tier 1 banking location — in particular, in relation to its anti-money laundering (AML) regime.

- The Austrian government aims to strengthen the FMA as regulator and is rolling out initiatives to attract new investors and businesses.

- In comparison to other Western European prime locations, Austria — next to its operational attractiveness — offers a good corporate governance and beneficial tax regime, including a benign corporate income tax level.

On the retail side, we saw the exit of ING and Sberbank’s exiting the Balkans while Bawag group acquired Hello Bank from BNP Paribas. There are rumors of further international banking groups considering an exit from the Austrian market.

How do you expect ESG scrutiny to change in deals over the next three years?

The awareness of ESG among clients, companies and investors has increased in recent years. In our view, ESG evaluations — be it for diversifying investment portfolios or improving corporate image — will become more and more important.

Against the background of the increased interest and relevance of sustainability criteria, ESG due diligence (DD) is more often requested in M&A transactions. Traditional financial or tax DDs are supplemented by "soft" factors such as environmental, social or organizational aspects. Such soft factors can have a decisive influence on the accuracy of the valuation of the target.

Possible advantages of an ESG DD arise from the uncovering of reputational risks, the identification of (future) liability risks, the determination and, if necessary, quantification of value-enhancement potentials and, finally, the resulting costs that could arise after the acquisition of the target.

Investors may consider ESG factors in their investment decisions in addition to more common financial variables. An ESG DD reveals additional arguments for purchase price negotiations and forms an additional basis for a company valuation.

The scope of an ESG DD has to be based on an investor’s preferences, values and ethics. It often determines which companies, sectors or activities are eligible or ineligible to be included in a specific portfolio. Most screening methods try to avoid or exclude the largest greenhouse gas emitters in a portfolio (negative screening).

What will be most important to help banks better execute M&A in 2022?

In our experience, two aspects are key to a lean and swift banking M&A transaction:

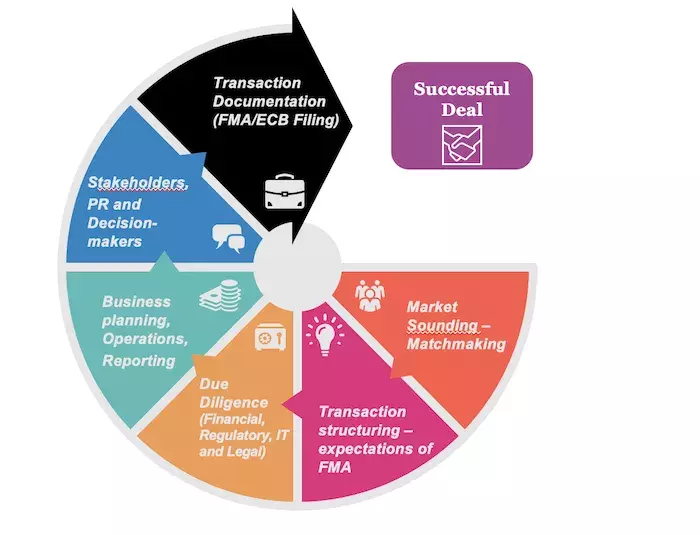

1. Early involvement of lawyers and advisors: Banking M&A deals tend to be of relatively high complexity. The regulatory assessment of a potential transaction and the expectations of the national competent authorities as well as the ECB are key to the success of a transaction. It usually centers around sustainable business models, ensuring continued operations (core banking systems and operational risks) as well as the fit and properness of the new owners.

Sell-side as well as buy-side transactions need to be structured accordingly to address the expectations of the regulator from the beginning.

Buyers are advised to assess their own fit and properness which may also require substantial preparations such as identification of the appropriate acquisition entity, source of funds, business model, financing of the transaction or future reporting and consolidation (financial and regulatory). Buyers should engage their advisors during the market sounding phase when deciding in which market or country they wish to become active.

On the sell-side, the structuring entails an appropriate disentanglement from group functions as well as ensuring day-one readiness of the target after closing the transaction and corresponding transitional services. The selection of the appropriate buyer will largely depend on the success of a buyer to obtain ownership-control approvals from regulators.

2. Definition of a lead advisor: Banking M&A requires the coordination of various workstreams that go beyond mere legal, regulatory and financial aspects and also include IT, HR, PR and public stakeholder management.

The lead advisor should be mandated as early as possible in the transaction. When we are entrusted with such a mandate, our goal is to take as much burden off the client's shoulders as possible. The lead advisor acts as sole point of contact with the client and sub-engages additional advisors where needed. Ideally, the lead advisor is independent and not restricted by network rules. They should source the best experts from various IT and financial advisory firms such as the Big Four and negotiate pricing in the client’s favor.

Summing up, we expect a very active banking M&A market in Austria in the coming years. Banking M&A remains to be a challenging transactional market with complex regulatory processes which require advisors to have a deep understanding of banking supervisory mechanics, business planning as well as banking processes. In our view, a combined legal, regulatory and financial advisory team approach is key to success. If implemented from an early stage on, will significantly enhance the chances of getting the deal through. Our transaction circle visualizes our PHH approach: