Private Credit Takes Center Stage on LPs' Investment Radar

The higher interest rate environment has boosted private credit’s appeal to allocators.

Interest in private market investments has grown significantly since the Global Financial Crisis, with private equity garnering most of the inflows. More recently, however, private credit has captured the attention of limited partners (LPs).

This prevailing sentiment was reflected in the findings in the SS&C Intralinks 2024 LP Survey, produced in association with Private Equity Wire, which gathered insights from 251 globally based LPs on a range of topics.

In one of the headline findings, a vast majority of respondents (71 percent) believe that private credit funds will assume a significantly greater role in the industry over the next 12 months.

The sentiment resonating on Wall Street is unanimous. Marc Pilgrem, BlackRock’s EMEA head of family offices, said private credit was “drawing big interest in this higher-rate environment.”

Forty-two percent of respondents to the U.S. firm’s recent family office survey were planning a higher exposure — double the 21 percent planning increased allocations to hedge funds.

Prominent LPs, such as the University of California’s investment fund, have said they will stop betting on hedge funds to allocate more capital toward private credit.

“Within two or three years, whenever we can get liquidity from our hedge funds, we will be primarily all out,” said University of California CIO Jagdeep Bachher at an investment meeting earlier this year, calling private credit “a better place to be.”

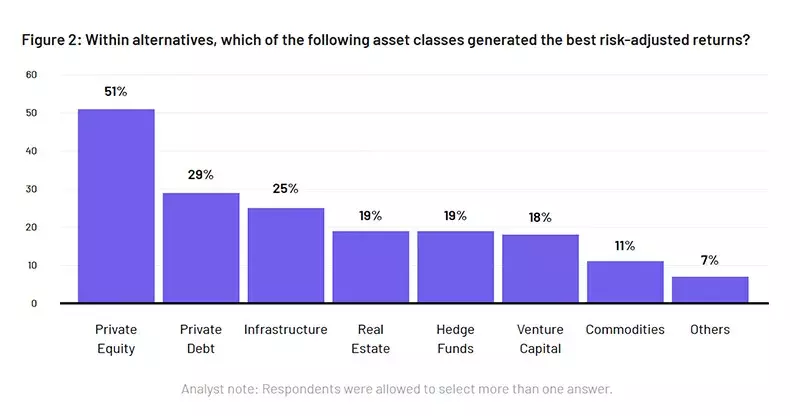

Assessing the performance of private credit, our survey underscores that private equity emerged as the leading source of performance satisfaction in the previous year, closely trailed by private debt/credit, Infrastructure and Real Estate. In terms of satisfaction, hedge funds secured the fifth position, just slightly behind private asset classes. This observation could potentially serve as an indicator influencing future allocation trends.

Looking ahead, however, there is an expectation private credit can outperform the rest. Recently, Citi Private Bank published its Global Family Office Report 2023, which added context about allocator interest in private credit.

Family offices were more positive on private credit than private equity, with 44 percent saying they were bullish on the former against 32 percent who were bullish on PE funds.

It is something of a scale play, with larger family offices more likely than smaller ones to be planning to add to private credit (55 percent versus 31 percent).

What is behind the interest? “We believe private credit managers may see equity-like returns in debt markets over the next three to five years,” wrote the authors of the report. “As 2024 comes into focus, we see potential yields of 5.5 to 10 percent available across investment grade through private credit assets. Family offices can thus seek to preserve wealth with yields that may exceed long-term inflation rates.”

Kathryn Saklatvala, senior director, head of investment content at investment consultancy bfinance, says she is seeing rising interest in private credit on both the corporate lending side and relating to “real assets” like real estate or infrastructure debt.

“Even with the rise in base rates, the illiquidity premium has been maintained and may even have increased,” she says. “Investors have also noted the resilience of private credit in the last twelve months of turmoil, with default rates staying low.

“A retrenchment in bank lending and volatility in public markets are supporting strong demand from borrowers — companies that need refinancing or are changing hands. It’s worth giving special mention to real estate debt: USD 1.5 trillion of senior loans are expected to need refinancing in the U.S. alone over the next three years.”

She adds that LPs should keep a close eye on fees in the asset class. “Asset managers are getting more attractive terms but, where hurdle rates are low [a legacy of a low interest rate climate], managers will take a larger proportion of those returns out via performance fees.”

Trends in Private Credit Fund Structuring, a new survey conducted by the trade group Alternative Credit Council (ACC) and law firm Dechert, revealed how managers are increasing their use of customization in private credit in response to greater LP interest.

“Private credit is a permanent fixture in the allocation models of many global investors,” said Jiří Król, head of the ACC. “Customized structures play an important role in accommodating this demand for ongoing exposure to private credit strategies and ensures that investors can tailor exposure according to their risk appetite.”

According to the ACC/Dechert survey, a significant majority of respondents, precisely four-fifths, navigate their capital allocation landscape through a combination of commingled funds and various other vehicles. While the lion's share of capital devoted to private credit strategies finds its home in commingled structures, an overwhelming 95 percent of respondents extend the option of managed account structures tailored to individual investors.

“Our research indicates that there is growing demand from investors for tailored investment structures and private credit managers see being able to meet this demand as strategically important,” the report added.

Another key finding showed that investor demand for permanent capital allocations to private credit strategies is being met by fund structures that offer partial liquidity. Half (51 percent) of respondents offer their investors some form of right to redemption and 48 percent expect investor demand for liquidity to increase in 2023.

Conclusion

The buzz surrounding private credit has been impossible to overlook in recent months. Our survey underscores that these headlines are not just buzz; they are substantiated by the sentiments of LPs, with nearly three-quarters envisioning a significantly expanded role for this sector in the coming year.

Industry surveys echo this trajectory, revealing that private credit is attracting more interest even than private equity, one of the hottest areas of finance for years. General partners (GPs) are actively responding to this heightened LP demand by offering greater customization in their offerings, allowing tailored approaches to investment.

As the private credit asset class continues to expand, there will inevitably be increased scrutiny on fees and other aspects. Nevertheless, GPs should be prepared to rise to these challenges in the coming years.

The 2024 SS&C Intralinks LP Survey is available to download here.